Further interest rate hikes expected from the Bank of England

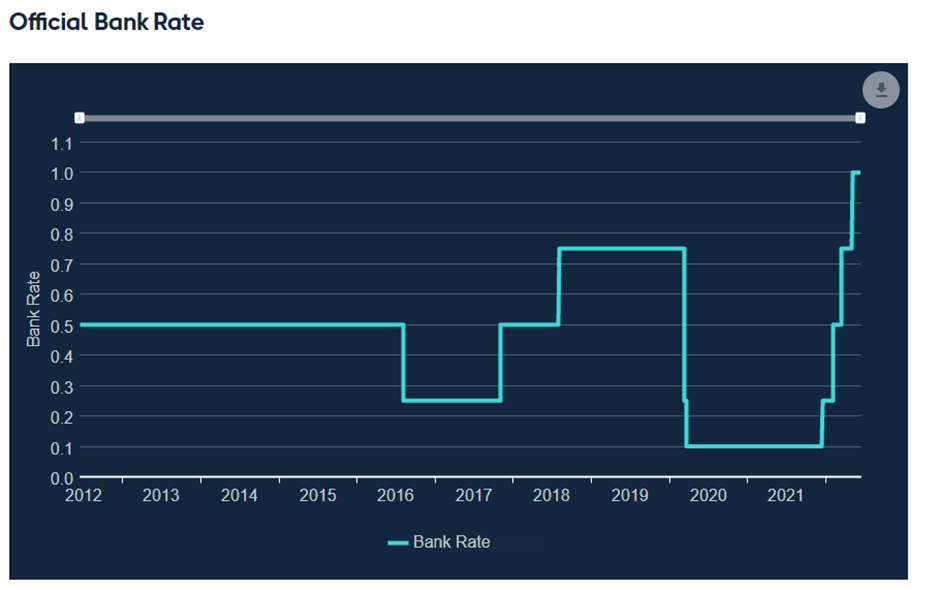

On Thursday 16th of June 2022, the Bank of England will once again meet to discuss interest rates. Analysts are expecting a rise from the current rate of 1% to either 1.25 or 1.5%.

If this move is made, then it will the first time that it’s been over 1% since January 2009. The Monetary Policy Committee (MPC), who set the rate, will announce their decision tomorrow.

What is the Base Rate?

The Base Rate, sometimes called the Bank Rate determines the interest rate the Bank of England pays to commercial banks that hold money with them. It also influences the rates that these banks will charge people to borrow money or pay them on their savings.

It is the single most important rate in the UK.

How does this affect us individually?

When the Bank Rate changes, normally banks will change their interest rates on saving and borrowing. Whilst it isn’t the only factor that influences this, it’s certainly an important one.

Interest rates change for a multitude of reasons and the changes seen in the commercial banks rates may not be the same as the change to the Bank Rate. For banks to stay viable, they need to pay less on saving than they make on lending.

How the rate changes affect you largely depends on whether you are saving or borrowing.

If rates fall and you have a mortgage, your repayments may become cheaper. Conversely, if the Bank Rate is increased, then you will likely see your repayments becoming more expensive.

When will the Bank of England make their decision?

The Bank of England is due to meet on this tomorrow (16th June 2022) and have the following dates in the diary to discuss it again:

- 4th August 2022

- 15th September 2022

- 3rd November 2022

- 15th December 2022

Why are they increasing interest rates?

The Bank of England has a wide range of responsibilities and acts as the governments bank and lender of last resort. One of their responsibilities is to keep inflation in check.

Inflation rates are currently the highest they have been since April 1991, and the economy cannot really afford for them to increase much higher. Inflation devalues money as the cost of goods and services increase, meaning we get less product for the money we spend. You will relate to this if you have filled your car up recently.

The Bank of England will increase the base rate which will in-turn drop the demand for spending and increase the desire to save money instead. In turn, this should help bring the costs down as the demand for these products the subsides.

If you still aren’t sure how this works, then this extract from the Bank of England’s website should help:

Overall, we know that if we lower interest rates, this tends to increase spending and if we raise rates this tends to reduce spending. So, to meet our inflation target, we need to judge how much people intend to save and spend given the current interest rates. For example, if people start spending too little, that will reduce business and cause people to lose their jobs. In that case we may cut interest rates to help support spending

Is increasing the Bank Rate the right move?

To be truthful, we don’t really know. We can only trust that the Bank of England have a plan of action and are taking the best steps and precautions that we need them to.

It is widely feared that increasing the rates too far could mean disaster for our already fragile economic recovery coming out of the pandemic and tip us into a recession.

One thing we do know, is that if the Bank of England increased the base rate further, then mortgage lenders will likely increase their rates too.

Will it be harder to get a mortgage?

At Prospect Tree Mortgages, we quiz our lenders each day to find out what their plans are moving forward. Not only are we concerned about rising rates, but the affect that this will have on borrowers’ affordability and how much they can ultimately borrow.

Our mortgage experts have their finger firmly on the pulse and despite these challenging times, are still here to help you find the best mortgages available to you and your circumstances.

With access to the entire UK mortgage marketplace, we can help you gain access to the best mortgage for your situation and help you make savings wherever possible.

Mortgage reviews are important and now is certainly the time to do it. Delay doing this and you will end up paying more interest than you need to.

It’s important to remember that a higher mortgage payment due to a higher interest rate doesn’t mean you’ll pay off your mortgage more quickly. The extra interest you pay will be taken by the bank and that’s the last you’ll see of it.

Given the choice, would you not rather keep this money for yourself?

If you’d like to learn more about mortgage products and how we can help you, please don’t hesitate to get in touch with our team. We’re here to help you navigate the ever-evolving world of mortgages and guide you toward a brighter, greener home.

<div data-tf-widget=”F08kvF4f” data-tf-opacity=”100″ data-tf-iframe-props=”title=Prospect Tree Mortgages – How can we help you?” data-tf-transitive-search-params data-tf-medium=”snippet” style=”width:100%;height:500px;”></div><script src=”//embed.typeform.com/next/embed.js”></script>